In April, inflation continued to be the main narrative as global inflation data posted multi-decade highs, and global central banks started hiking aggressively. Expectations for more hawkish Fed hikes have reached three 50-basis points hikes and a total of 275 basis points of tightening to year-end. If the Fed can deliver such an aggressive, brute force attack on inflation, it may likely lead to collateral damage and consequences.

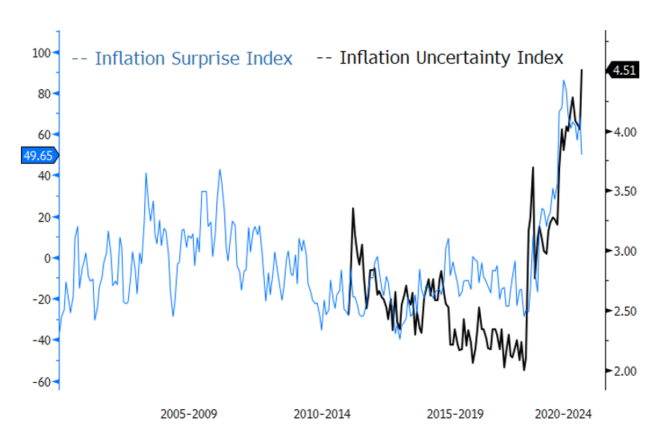

But with 8.5% inflation, a little demand destruction will not be sufficient. Despite the fixation and focus on inflation for more than a year, there is surprisingly little consensus on the inflation outlook. Figure 2 highlights that inflation surprises are still elevated and that the level of uncertainty is likely to continue to increase. Looking ahead, inflation and expectations will continue to rile markets.

Figure 2. Inflation Surprise Index and Inflation Uncertainty Index (2005-2022)

Source: Bloomberg and Sprott Asset Management LP. Data as of 4/30/2022. Included for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

… And Stagflationary Pressures Still Rising

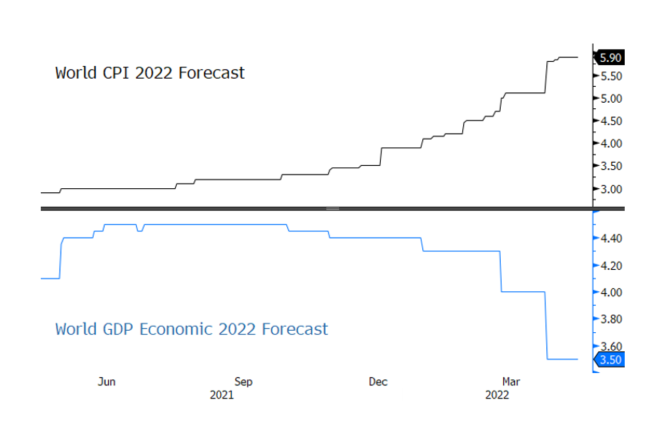

Global GDP saw further downward revisions for 2022. The IMF downgraded 2022 global GDP from 4.4% to 3.6% and the World Bank lowered its estimates from 4.1% to 3.2%. The effects of the Russia-Ukraine War, now entering its third month, continue to ripple through supply chains, commodity markets, trade and financial linkages. With few signs of a resolution or end, spillover effects will likely continue to accrue. Globally, inflation pressures continue to rise and inflation indices are reaching new all-time highs. Figure 3 highlights the growing global stagflationary stress: Rapidly increasing inflation expectations and GDP expectations tumbling.

Figure 3. Global Stagflation Pressure is Accelerating (2021-2022)

Source: Bloomberg and Sprott Asset Management LP. Data as of 4/30/2022. Included for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

Unprecedented Drawdown on Bonds

During the May 4, 2022, Federal Open Market Committee (FOMC) meeting, the Fed will announce its quantitative tightening (QT) or balance sheet runoff/reduction schedule. The expectation is that the runoff caps will be larger and quicker, and when combined with aggressive rate hikes, it will likely lead to a policy of tightening that is possibly greater than what the market is expecting. QT is likely to be a massive change in the flow of funds in and out of U.S. Treasuries, affecting every asset class.

In short, QT will lower the tipping point of a potential overshoot in Fed rate hikes. The expected fastest rate hike since 1989 (0 to 300 basis points in 12 months, including three 50 basis point rate hikes) plus QT is an off-the-charts level of tightening and this will likely impact equities, credit and especially bonds. Mortgage-backed securities (MBS) runoff remains an underappreciated risk as the Fed may target home prices to reign in inflation and inflation expectations more quickly. As we mentioned before, an aggressive MBS runoff runs a high contagion risk to credit market risk because of its spread product nature.

The U.S. Treasury Index's YTD 2022 return is now -8.5%, representing a significant loss in the value of U.S. government bonds. But it is the drawdown that highlights the pressure facing most multi-asset funds. The drawdown is the worst in nearly 50 years, at twice the prior maximum drawdown levels ever experienced (see Figure 4). Bonds typically function as a hedge or protective asset in multi-asset portfolios. Global bond aggregates are experiencing even worse drawdowns (-15.48%), highlighting the dearth of safe-haven assets.